Nicola Willis's fiscal poetry contest

Calling all creative writing graduates.

As an English lit grad, New Zealand’s finance minister Nicola Willis will be needing inspiration ahead of Election 2026.

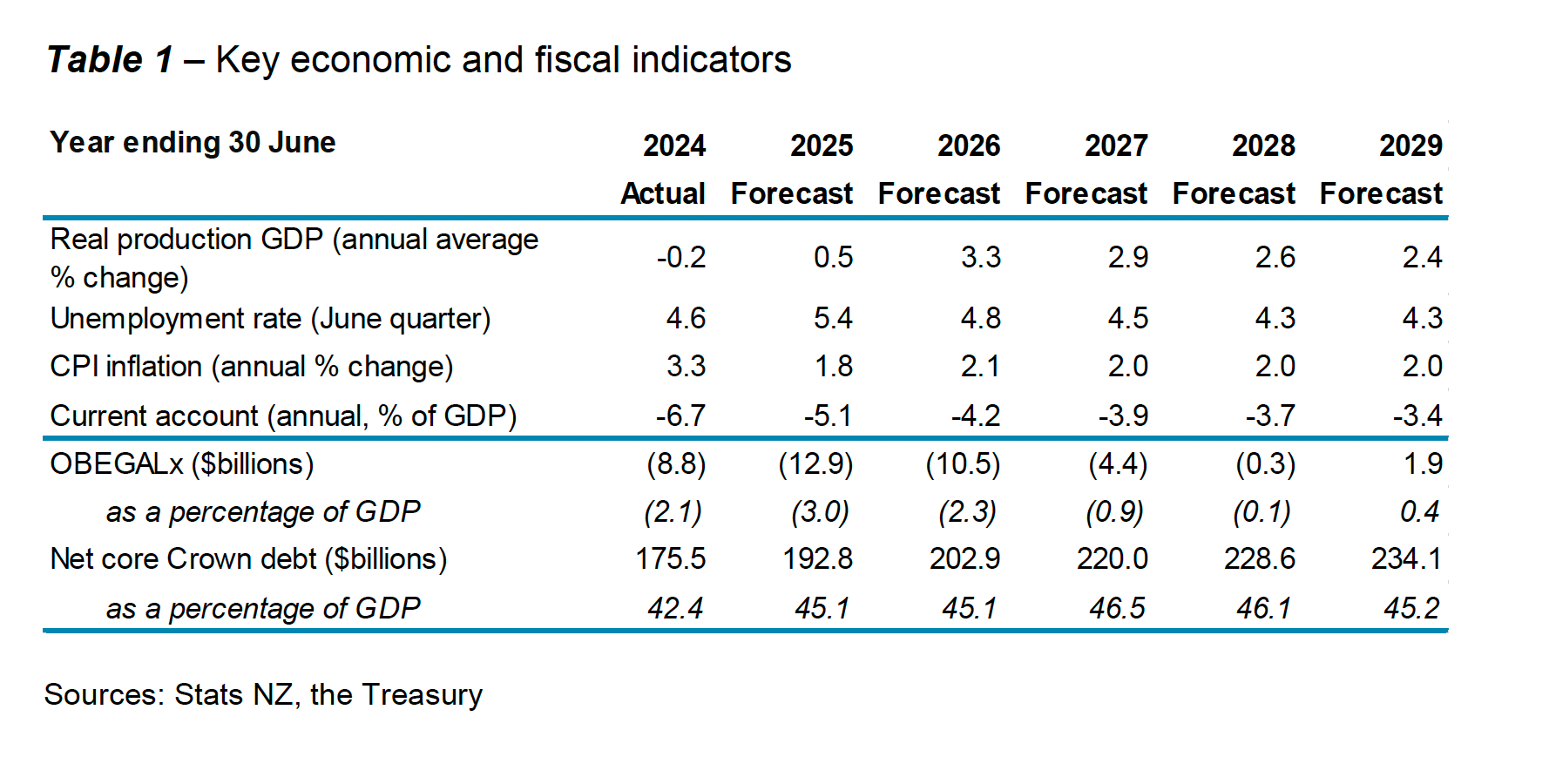

On Tuesday, with the release of the half-yearly economic and fiscal update (HYEFU), Willis was copping criticism from left and right, with accusations of “creative accounting” and “cooking the books”. The target of these jibes is the government’s new headline debt indicator – the operating balance before gains and losses excluding Accident Compensation Corporation (ACC), or OBEGALx.

Before the lefties get too excited, though, let’s recall that Labour’s former finance minister, Grant Robertson, used an even bigger creative trick back in 2022 by switching to a measure of government debt that basically halved the headline number. And Willis’s sleight of hand could be defended (if you’re feeling generous) on the grounds that the ACC is valued separately on an actuarial basis: that is, it accounts for all outstanding claims liabilities, which stretch into the future, well beyond the HYEFU’s forecasting period.

Rather too conveniently, though, the OBEGALx (excluding ACC) is projected to return to surplus in 2028/29, while the previously used operating balance before gains and losses (OBEGAL including ACC) is forecast to remain in deficit over the entire forecast period with a deficit of $2.4 billion expected in 2028/29. (See HYEFU page 23.) This new turn of phrase makes things look less bad, in other words, but at least the Treasury makes it transparent.

It’s suddenly become convenient to exclude ACC because the Corporation reported (in November) that the Scheme’s funding ratios are worse than projected in their last annual report. Explainer: a funding ratio relates to all open claims. It’s the ratio of assets (mainly investments) over the estimated future liabilities arising from outstanding claims. As ACC should be fully funded, that ratio should be around 100%. The current shortfall means that ACC levies need to rise. But ACC also needs to reduce the time it’s taking to return injured people to work, while the present rise in unemployment affects its performance.

It’s not all bad news for Nicola, however. Official projections released by the Treasury – if they come true – suggest that she may be able to wax lyrical about economic growth before the next election. Treasury is forecasting 3.3% growth in the year to 30 June 2026.

It’s sadly true, on the other hand, that actual growth in the 2023/24 year was –0.2%, but political memories are as retentive as sieves. And anyway, that depressing figure can still be blamed on Labour.

When, in disgrace with fortune and men’s eyes,/I all alone beweep our fiscal state…

Willis’s line about “cleaning up the mess left by Grant Robertson” has a use-by date, which probably expired in October. So she’ll need some fresh similes for her live tour scheduled for spring 2026.

Now, I’ll make a prediction that, at least once in that campaign, Christopher Luxon will go: “What I’d just say to you is that there’s no magic money tree at the bottom of the garden”. It’s a bit stale, but always an audience pleaser – at least for the blue side. And National’s reinstatement of tax-deductible mortgage interest for landlords was a gift to a tiny minority that all New Zealanders now have to pay for through interest on a public debt that will consequently be higher, and for longer, than it would otherwise have needed to be.

Avenge, landlord, thy unpaid rents, with homes/ where children suffer from the cold…

On Crown debt, National will need more creative genius than Shakespeare or Milton could supply.

Luxon & Willis’s pre-election fiscal plan stated: “Under National, the Government’s books are forecast to return to surplus in 2026/27”. The Treasury is now forecasting no budget surpluses until the 2028/29 fiscal year – two years late – even after Nicola’s creative rewriting.

When her political deadline arrives at the next election, though, how will Nicola explain that she’s nowhere near completing her pass-or-fail assignment?

In the two years to 30 June 2026, net core Crown debt is projected to grow from $175.5 billion to $202.9 billion. That would be a 15.6% increase – growing much faster than GDP. It may not compare with what happened under Labour in the wake of the Covid-19 fiscal stimulus, but it’s embarrassing for a political party whose pitch to voters was based on a reputation for being the most awesome of all economic managers.

How true is this of NZ politicians and the economy? “

“Risk comes from not knowing what you are doing.” Warren Buffett

It is strange how successive governments have put politicians with limited training in Economics or Accounting in charge of the finances. I wonder if this is because Minister of Finance is seen as a marketing role, not a position from which to develop innovative fiscal policy?